Today marks the day when leading payment processor PayPal opens up for cryptocurrency-powered business. A driving force in the crypto world, PayPal is the next big company – after Square – to see the potential in cryptocurrencies and adapt.

Crypto License Granted

Following the first “conditional BitLicense” granted by the New York State Department of Financial Services, PayPal Holdings Inc. has teamed up with Paxos Trust Company – allowing customers to pay and be paid in cryptocurrencies using one of the most popular household names in the world of payments.

The DFS’s superintendent – Linda A. Lacewell – stated that this development is a direct result of their new approach to cryptocurrencies. Hoping to attract entrepreneurs and businessmen with a cutting-edge vision, cryptocurrencies were naturally a major area of interest.

“DFS’s approval today follows our June 2020 announcement for a new framework for a conditional Bitlicense to encourage, promote, and assist interested institutions to have a well-regulated way to access the New York virtual currency marketplace in a way that is both timely and protective of New York consumers, through partnerships with New York authorized virtual currency firms.”

With over 26 million merchants and 325 million customers worldwide, this is a welcome addition for anyone who needs to make payments online. Other projects – such as the pending Cardano integration for Shopify stores are also bringing eCommerce and cryptocurrencies closer every day.

Although PayPal only provides support for cryptocurrencies in the USA for now, the first half of 2021 should bring the service to other markets worldwide – with Australia and the European Union among the chief markets targeted.

The cryptocurrencies supported initially will be Bitcoin, Ethereum, Bitcoin Cash, and Litecoin – although support for more cryptocurrencies should be added in the future.

Arbitrage is the market behaviour of taking advantage of the market economy’s imperfect price system to get additional profits through buying and selling. Arbitrage helps financial markets operate effectively, improves the asset pricing efficiency, and increases the market liquidity all at once.

The whole cryptocurrency industry is in its infancy. The entire trading market still lacks a comprehensive trading system and regulatory measures. Therefore, the arbitrage space is broad. Let us see how popular DeFi projects do arbitrage.

DeFi arbitrage usually stands for borrowing at low interest rates in one DeFi market and depositing assets to another DeFi market to earn high interest rates. When there is a positive gap between the deposit and borrowing rates, arbitrage opportunities appear.

Unlike the traditional arbitrage, DeFi uses the interest rate gap of cryptocurrency products to make profits instead of directly using the price difference of the underlying assets. Generally, DeFi market interest rates are relatively high. Here is why.

Decentralized Finance protocols are new. Factors like high volatility of cryptocurrencies, over-collateralization, and smart contract risks are all risks that define high interest rates. Similarly, funds deposited to the lending market of traditional finance bear lower risks. DeFi market needs to leverage high interest rates to make up for the risk brought by decentralized mechanisms.

High interest rates help the cold start of some new DeFi projects. Currently, most of the funds are in the mature DeFi markets with liquidity mining. Some new projects have not yet issued governance tokens and cannot provide liquidity incentives, resulting in poor early liquidity, so high interest rates can be useful. This also allows for more arbitrage opportunities between DeFi markets when the user base expands.

Detailed Arbitrage Process

For example, the annual interest rate of USDC loans on Compound is 6.07% while the annual deposit rate is only 2.21%. At the same time, USDC deposit interest rate on Nuo Network is as high as 11.8%.

Thus, holders of the same cryptocurrency USDC can choose to borrow on Compound and deposit to Nuo Network. If the interest rate stays the same, annualized profit is 5.73% (no fees and other costs included) and there is quite an arbitrage space.

Another high-level DeFi arbitrage method is to borrow ETH (which has the lowest loan interest rates in one market) on Compound, exchange it to USDC (which has the highest deposit interest rate in another market) and deposit to Nuo Network to get a higher annualized return of 9.19%. Eating the spread between deposits and loans on different platforms equals to risk-free arbitrage.

Among the new DeFi projects, strategies of some are more aggressive. Take the aggregated InfinityDefi (INFI) for example. It is similar to Compound, except that its arbitrage space and lending functions are richer and more flexible than those of early collateral projects.

Besides collateral lending, InfinityDefi protocol has an adjustment mechanism in its fund pool (dubbed Polymerization Pool or PP) to dynamically adjust interest rates along with the changes of currency ratios, so that supply and demand of any currency are balanced. When users borrow some currency, they pay interest. When users pledge (deposit) some currency, they earn interest. The higher the supply and demand, the higher the interest rates.

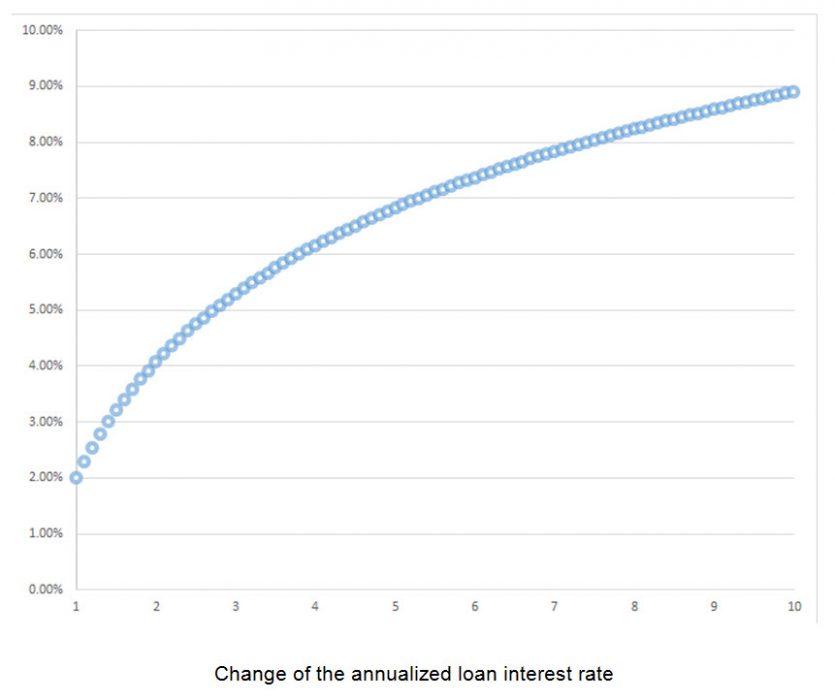

x axis is the total non-lent market value of the fund pool divided by the non-lent market value of currency i, range is 1 to 10. y axis is the corresponding annualized interest rate.

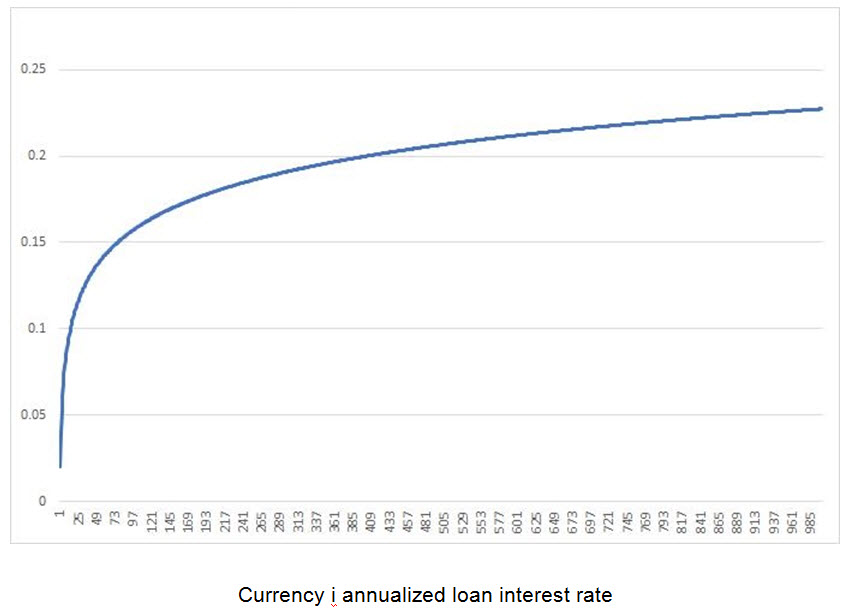

x axis is the total non-lent market value of the fund pool divided by the non-lent market value of currency i, range is 1 to 1,000. y axis is the corresponding annualized interest rate.

Example: a user wants to borrow ETH of 10,000 USDT market value. What is the current annualized interest rate for ETH?

The total non-lent market value of the fund pool is 100,000,000 USDT. The current market value of non-lent ETH is 10,000,000 USDT. Then, M(ETH) = ln10 = 2.303

The current annualized interest rate for ETH loans is min(2%+3%*2.303, 200%) = 8.9%.

Then what interest can user A earn if the market value of ETH it deposited is 10,000,000 USDT?

The total market value of ETH pledged in the fund pool is 200,000,000 USDT.

Users B and C each borrowed ETH worth of 50 million USDT and no other users borrowed ETH. User B pays 600 USDT interest for the past 1 hour (as per the formula for the interest on borrowing) and user C pays 800 USDT interest for the past 1 hour (because B and C borrowed ETH at a different rate). Thus, A’s accrued interest for the past hour is 10,000,000*(600+800) /200,000,000 = 70 USDT.

3. How to Use INFI’s Low Borrowing Rate for Low-risk Profit

According to INFI’s dynamic interest rate algorithm, INFI collateralized loan interest rate is quite low. With its low interest rate for mainstream coins (4%) INFI attracts borrowers who then deposit these coins on other platforms with higher deposit rates (say, 7%)*. This is the low-risk spread arbitrage. Profit!

*Comparing to the data collateralized DeFi deposit interest rates by Feixiaohao, September 24, 2020

What sets InfinityDefi and traditional DeFi apart:

INFI has the regular collateral lending. What’s more, users can do secondary collateral. That is, you can pledge your collateral agreements from other platforms. This gives you a better arbitrage space. INFI also has multi-value-added loans (MVA). When the value of your collateral increases (the price of the locked coin rises), you can also pledge this value-added part to increase your collateral multiple times and thus get more loans.

INFI is lower pledge ratio (around 5% compared to traditional DeFi), higher loan amounts (20% compared to traditional DeFi), and faster capital turnover.

An example of a secondary loan: one platform, ETH and USDT. A is a borrower with primary and secondary collateral. B is the secondary collateral pool under PP.

A pledges ETH with a market value of 1.45 USDT, gets a loan of 1 USDT from the InfinityDefi Protocol, and pays a 5% interest (see the payable interest formula). A needs short-term funds. It transfers the pledge agreement to B, becomes the borrower with secondary collateral, gets a secondary loan of 10% of the primary loan (0.1 USDT), and pays a 7% interest (see the payable interest formula). B only lends 0.1 USDT to get a collateral agreement with a 7% interest.

For redemption, A pays 0.1 USDT plus interest and redeems the agreement from B. Then A pays 1 USDT plus interest and redeems ETH from the Protocol.

Position coverage is required at 145%. When ETH price falls and the pledge ratio is below 1.45, A needs to cover the position within the defined time.

Liquidation happens at 125%. When ETH price continues to fall and the current pledge ratio is below the minimal level (125%), liquidation starts. The Protocol liquidates at the current market price and B gets the remaining ETH (if any) after the payment of the principal of 1 USDT + interest + liquidation fee (8%).

If B fails to pay, the platform liquidates the collateral at the market price to repay B’s debt / Protocol debt and the 8% liquidation fee. The remaining balance returns to A.

PPT (equity token) and INFI (governance token)

User earn PPT for each loan and primary/secondary collateral. PPT has decentralized generation and distribution. PPT rewards depends on the amount and duration of the respective collateral or loan. Users can exchange PPT to INFI, the latter one will hit mainstream exchange platforms.

You may have noticed the industry trend. The requirements for investors are getting higher and higher in terms of both time and knowledge. When public chains appeared, you probably knew the basic concepts like PoW, DPoS, and TPS. Now it’s the next level and you have to understand channels, side chains, rollups, parachains, shards, cross-chain… the endless list of new things, each one running on its own new consensus mechanism.

Similarly, in the early days of DeFi, it was just DEX, decentralized trading, and borrowing. Now you have to understand liquidity, AMM formulas, derivatives, stablecoins, liquidation, aggregation… plus everything that the next level of public chains has brought about because many new DeFi products will soon be available on ETH 2.0 and new public chains like Polkadot and Solana that are about to launch.

The current blockchain DeFi needs you to be good at both blockchain and finance. This is the fastest growing space now knowledge and opportunity-wise.